Social finance is evolving just as quickly as climate finance, and maybe even under more complex constraints. Having reviewed applications for the upcoming ISFA cohort, a few clear patterns are emerging. They do not point to a single dominant model, but rather to a sector actively testing its boundaries. Heading into 2026, these are the social finance trends we are watching most closely.

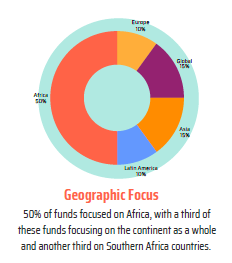

Prediction 1: Africa remains the centre of gravity, but not in a single shape

Half of ISFA applicants focus on Africa, confirming the continent’s continued centrality to social investment strategies. What is striking is not only the scale, but the internal differentiation: a meaningful share of Africa focused funds are continent wide, while an equally large group concentrates specifically on Southern Africa.

Analytically, this raises questions about execution risk. Pan African mandates might offer narrative scale, but regionally anchored strategies may be better positioned to demonstrate early proof points and operational depth.

Prediction 2: Global Mandates? Yes, but with Social trade-offs

Alongside region specific strategies, we see a notable share of funds positioning themselves as global across emerging markets, (framed around ODA eligible countries) rather than a single geography. These mandates reflect ambition and, in some cases, the need to diversify risk across contexts. At the same time, global social mandates remain difficult to execute, as unlike climate finance, social outcomes are deeply embedded in local systems, institutions, and norms.

In other words, without strong thematic or delivery anchors, global mandates can struggle to show depth of impact alongside breadth.

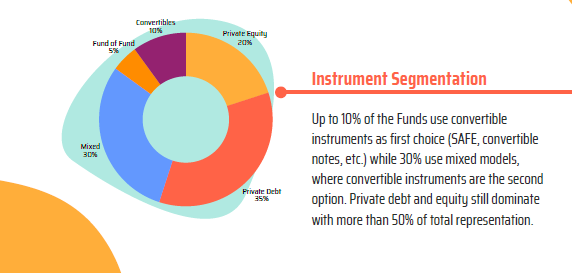

Prediction 3: Convertibles are entering Social Finance

Convertible instruments are no longer exclusive to venture or climate innovation. Around 10 percent of ISFA applicants use convertibles as their primary instrument, and a much larger share incorporates them as a secondary option alongside debt or equity.

In social finance, this reflects a search for flexibility in contexts where revenue visibility, policy risk, and impact timelines rarely align neatly. Hybrid structures such as debt combined with Simple Agreements for Future Impact, or others, are starting to make their way out.

Prediction 4: Traditional instruments still dominate

Despite growing experimentation, private debt and equity remain the backbone of social fund design, representing over half of all strategies. This is not conservatism so much as recognition of the environments social funds operate in: regulated sectors, essential services, and delivery models that often require predictable cash flows and patient capital.

What is changing is not the instruments themselves, but how they are layered with impact incentives and convertible instruments, blended capital, and technical assistance. This reality might suggest that innovation in social finance may be less about new instruments and more about smarter structuring, sequencing, and risk sharing.

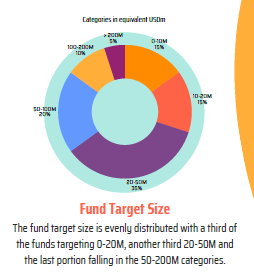

Prediction 5: Fund sizes are diverging, not converging

Rather than clustering around a single “emerging manager” fund size, ISFA applicants are spreading across three distinct bands. Roughly a third of applicants are targeting funds below €20 million, often structured as pilots, first time vehicles, or proof of concept strategies. Another third cluster in the €20–50 million range, reflecting a more conventional first fund size. The final third are targeting significantly larger vehicles, from €50 million up to and beyond €200 million.

Within this upper band, funds targeting €50–100 million alone represent around 20 percent of the total applicant pool. Taken together, this means that approximately half of all ISFA applicants are designing funds between €20 million and €100 million, suggesting a growing middle ground between experimentation and institutional scale.

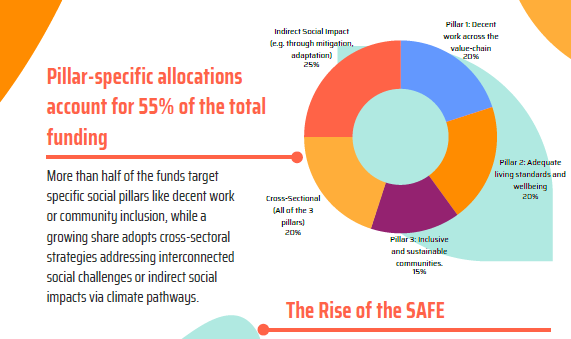

Prediction 6: Pillar-specific social funds still form the backbone

More than half of applicants focus explicitly on one of the three social pillars: decent work across value chains, adequate living standards and wellbeing, or inclusive and sustainable communities. Rather than disappearing, these focused strategies remain central to the social finance ecosystem.

Their strength lies in clarity. Clear beneficiary definitions, outcome pathways, and stakeholder alignment often make these funds easier to evaluate, support, and scale.

Prediction 7: Cross sectoral social strategies are gaining ground

One fifth of applicants position themselves as explicitly cross sectoral, addressing all three social pillars rather than specializing narrowly. These funds often frame social challenges as interconnected systems rather than siloed outcomes. This approach aligns with how people experience inequality and vulnerability in practice, where employment, living standards, and community resilience reinforce one another.

Although, without clear prioritization and impact measurement, this approach risks becoming conceptually inclusive but operationally diffuse.

Prediction 8: Indirect social impact rises

A quarter of ISFA applicants pursue social outcomes indirectly, through climate adaptation, mitigation, or other pathways. This reflects the growing recognition that climate and social risks are interconnected, particularly in vulnerable contexts. At the same time, indirect social impact introduces complexity. Demonstrating causality, attribution, and additionality becomes harder as social outcomes sit one step further from the core investment thesis.

While indirect social impact can be an opportunity it can also easily translate into potential dilution, as it can become a proxy for social impact without accountability.